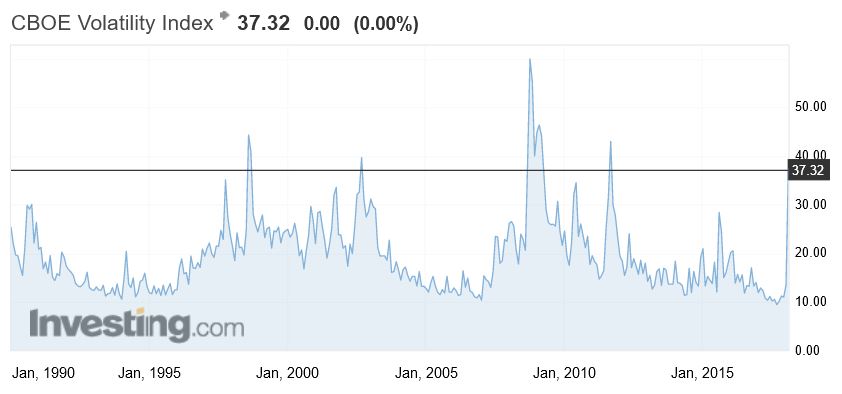

The volatility index (VIX) has roared back to life, having been asleep for months. This index gives an indication of market sentiment and is a popular measure of the stock market’s expectation of volatility implied by S&P 500 index options. This volatility is meant to be forward looking, is calculated from both calls and puts, and is a widely used measure of market risk, often referred to as the “investor fear gauge.”

On this basis, fear is stalking the halls, only 4 times since 1990 has the VIX index been higher.

The Home Price Crunch is happening now, but how low will prices go and which areas will get hit the worst? Welcome to the Property Imperative Weekly to 3rd February 2018.

Welcome to our digest of the latest finance and property news. Watch the video or read the transcript.

There was lots of new data this week, after the summer break. NAB released their Q4 2017 Property Survey and it showed that property dynamics are shifting. They see property prices easing as foreign buyers lose interest, and a big rotation from the east coast. Tight credit will be a significant constraint. National housing market sentiment as measured by the NAB Residential Property Index, was unchanged in Q4, as big gains in SA and NT and WA (but still negative) offset easing sentiment in the key Eastern states (NSW and VIC). Confidence levels also turned down, led by NSW and VIC, but SA and NT were big improvers. First home buyers (especially those buying for owner occupation) continue raising their profile in new and established housing markets, with their share of demand reaching new survey highs. In contrast, the share of foreign buyers continued to fall in all states, except for new property in QLD and established housing in VIC, with property experts predicting further reductions over the next 12 months. House prices are forecast to rise by just 0.7% (previously 3.4%) and remain subdued in 2019 (0.8%). Apartments will under-perform, reflecting large stock additions and softer outlook for foreign demand.

Both CoreLogic and Domain released updated property price data this week. It is worth comparing the two sets of results as there are some significant variations, and this highlights the fact that these numbers are more rubbery than many would care to admit. Overall, though the trends are pretty clear. Sydney prices are sliding, along with Brisbane, and the rate of slide is increasing though it does vary between houses and apartments, with the latter slipping further. For example, Brisbane unit prices have continued their downward slide, down to $386,000; a fall of 2.2 per cent for the quarter and 4.4 per cent for the year. Here units are actually at a four-year low. Momentum in Melbourne is slowing though the median value was up 3.2 per cent to $904,000 in the December quarter, according to Domain. Perth and Darwin remains in negative territory. Domain said Darwin was the country’s worst performer with a 7.4 per cent drop in its median house price to $566,000 and a 14 per cent plunge in its unit price to $395,000, thanks to a slowing resources sector. It also hit Perth, with a house median fall of 2.5 per cent to $557,000, and its units 1.7 per cent to $369,000. On the other hand, prices in Hobart and Canberra are up over the past year and Hobart is the winner, but is it 17% or 12%, a large variation between the two data providers? And is Canberra 8% or 4%? It depends on which data you look at. Also, these are much smaller markets, so overall prices nationally are on their way down. My take out is that these numbers are dynamic, and should not be taken too seriously, though the trend is probably the best indicator. Perhaps their respective analysts can explain the variations between the two. I for one would love to understand the differences. The ABS will provide another view on price movements, but not for several months.

The latest ABS data on dwellings approvals to December 2017 shows that the number of dwellings approved fell 1.7 per cent in December 2017, in trend terms, and has fallen for three months. Approvals for private sector houses have remained stable, with just under 10,000 houses approved in December 2017, but the fall was in apartments, especially in NSW and QLD. More evidence of the impact of the rise in current supply of apartments, and why high rise apartment values are on the slide. Also, the ABC highlighted the fact that Real estate sales companies are using big commissions to tempt mortgage brokers, financial planners and accountants to sell overpriced properties to unsuspecting clients. This is a way to offload the surplus of high-rise apartments, and looks to be on the rise, another indicator of risks in the property sector.

In other economic news, the ABS released the latest Consumer Price Index (CPI) which rose 0.6 per cent in the December quarter 2017. Annual inflation in most East Coast cities rose above 2.0 per cent, due in part to the strength in prices related to Housing. This follows a rise of 0.6 per cent in the September quarter 2017. However, there were some changes in methodology which may have impacted the results. Softer economic conditions in Darwin and Perth have resulted in annual inflation remaining subdued at 1.0 and 0.8 per cent respectively. Many commentators used this data to push out their forecast of when then RBA may lift the cash rate – but my view is we should watch the international interest rate scene, as this is where the action will be.

Whilst the FED held their target rate this week, there is more evidence of further rate rises ahead. Most analysts suggest 2-3 hikes this year, but the latest employment data may suggest even more. The benchmark T10 bond yield continues to rise and is at its highest since 2014, and now close to that peak then of about 3%. Have no doubt interest rates are on their way up. This will put more pressure on funding costs around the world, and put pressure on mortgage rates here. In fact Alan Greenspan, the former Fed Chair, speaking about the US economy said “there are two bubbles: We have a stock market bubble, and we have a bond market bubble”. “Irrational exuberance” is back! He said we’re working, obviously, toward a major increase in long-term interest rates, and that has a very important impact, on the whole structure of the economy. Greenspan said. As a share of GDP, “debt has been rising very significantly” and “we’re just not paying enough attention to that.” US rate hikes will lift international capital market prices, putting more pressure on local bank margins.

We published our latest mortgage stress research, to January 2018, Across Australia, more than 924,000 households are estimated to be now in mortgage stress compared with 921,000 last month. This equates to 29.8% of borrowing households. In addition, more than 20,000 of these are in severe stress, down 4,000 from last month. We estimate that more than 51,500 households risk 30-day default in the next 12 months, down 500 from last month. We expect bank portfolio losses to be around 2.7 basis points, though with losses in WA are likely to rise to 4.9 basis points. Some households have benefited from refinancing to cheaper owner occupied loans, giving them a little more wriggle room in terms of cash flow. The typical transaction has saved up to 45 basis points or $187 each month on a $500,000 repayment mortgage. You can watch our separate video blog on the results, where we count down the top 10 most stressed postcodes.

But the post code with the highest count of stressed households, once again is NSW post code 2170, the area around Liverpool, Warwick Farm and Chipping Norton, which is around 27 kilometres west of Sydney. There are 7,375 households in mortgage stress here, up by more than 1,000 compared with last month. The average home price is $815,000 compared with $385,000 in 2010. There are around 27,000 families in the area, with an average age of 34. The average income is $5,950. 36% have a mortgage and the average repayment is about $2,000 each month, which is more than 33% of average incomes.

We continue to see mortgage stress still strongly associated with fast growing suburbs, where households have bought property relatively recently, often on the urban fringe. The ranges of incomes and property prices vary, but note that it is not necessarily those on the lowest incomes who are most stretched. Banks have been more willing to lend to these perceived lower risk households but the leverage effect of larger mortgages has a significant impact and the risks are underestimated.

The latest data from The Australian Financial Security Authority, for the December 2017 quarter shows a significant rise in personal insolvency – a bellwether for the financial stress within the Australian community. The total number of personal insolvencies in the December quarter 2017 was 7,578 and increased by 7.4% compared to the December quarter 2016. This year-on-year rise follows a rise of 8.0% in the September quarter 2017.

This is in stark contrast to the latest business conditions survey from NAB. They say that the business confidence index bounced 4pts to +11 index points, the highest level since July 2017, perhaps driven by a stronger global economic backdrop and closes the gap between confidence and business conditions. Business confidence is strongest in trend terms in Queensland and SA and to a lesser extent NSW. Confidence is also reasonable in WA, and is in line with business conditions in the state. Victoria and Tasmania meanwhile are reporting levels of confidence which are lower than their reported level business conditions. But the employment index suggests employment growth may ease back from current extraordinary heights.

The RBA credit aggregates data reported that lending for housing grew 6.3% for the 12 months to December 2017, the same as the previous year, and the monthly growth was 0.4%. Business lending was just 0.2% in December and 3.2% for the year, down on the 5.6% the previous year. Personal credit was flat in December, but down 1.1% over the past year, compared with a fall of 0.9% last year. This is in stark contrast to the Pay Day Loan sector, which is growing fast – at more than 10%, as we discussed on our Blog recently (and not included in the RBA data). Investor loans still make up around 36% of all loans, and a further $1.1 billion of loans were reclassified in the month between investment and owner occupied loans, and in total more than 10% of the investor mortgage book has been reclassified since 2015.

The latest data from APRA, the monthly banking stats for ADI’s shows a growth in total home loan balances to $1.6 trillion, up 0.5%. Within that, lending for owner occupation rose 0.59% from last month to $1.047 trillion while investment loans rose 0.32% to $553 billion. 34.56% of the portfolio are for investment purposes. The portfolio movements within institutions show that Westpac is taking the lion’s share of investment loans (we suggest this involves significant refinancing of existing loans), CBA investment balances fell, while most other players were chasing owner occupied loans. Note the AMP Bank, which looks like a reclassification exercise, and which will distort the numbers – $1.1 billion were reclassified, as we discussed a few moments ago.

Standing back, the momentum in lending is surprisingly strong, and reinforces the need to continue to tighten lending standards. This does not gel with recent home price falls, so something is going to give. Either we will see home prices start to lift, or mortgage momentum will sag. Either way, we are clearly in uncertain territory. Given the CoreLogic mortgage leading indicator stats were down, we suspect lending momentum will slide, following lower home prices. We will publish our Household Finance Confidence Index this coming week where we get an updated read on household intentions. But in the major eastern states at least, don’t bank on future home price growth.

If you found this useful, do like the post, leave a comment or subscribe for future updates. By the way, our special post on Bitcoin will be out in the next few days, we have had to update it based on recent market gyrations.

The fall in the price of bitcoin continues, to a new 2018 low. More evidence of the volatility of this commodity, which further undermines its potential as a virtual currency. After all, the whole point of a currency is to have some relatively stable view on its value. Yelland’s “This is a highly speculative asset”, looks right.

Other major cryptocurrencies – including Ripple XRP, Ethereum and Bitcoin Cash – are also falling. Many of them are seeing more dramatic swings even than bitcoin.

A few factors are playing here. Facebook has banned cryptocurrency advertising on its platform.

There have been several bitcoin exchange hacks, including the now famous US$534m job on Coincheck.

And South Korea, one of the main trading centres, has banned anonymous trades, effective 30th January 2018. Also the country’s customs service says that around 637.5bn KRW (US$598.6m) worth of foreign exchange crimes have been uncovered. That said, South Korea is not planning to ban cryptocurrency trading, the country’s finance minister has said.

After China shut down the largest cryptocurrency exchanges last September, and also banned Initial Coin Offerings, Japan has taken on the mantle of bitcoin’s new capital, where strong interest in currency trading AND technology align. In fact Japan had 51% of global trading volumes in January 2018. Bitcoin is also recognised as a payment mechanism there, and regulators there have introduced measures to monitor transactions on the lookout for criminal activity.

Today Japan’s financial regulator on Friday swooped on Coincheck Inc with surprise checks of its systems and said it had asked the Tokyo-based cryptocurrency exchange to fix flaws in its computer networks well before hackers stole $530 million of digital money last week, one of the world’s biggest cyber heists.

German President Frank-Walter Steinmeier on Thursday warned the financial sector that it had a responsibility to prevent speculation and the formation of trading bubbles in the cryptocurrency market. Steinmeier told about 1,000 guests at a Deka Bank event in Frankfurt that a new debate was needed about regulating cryptocurrencies, given recent gyrations in their valuations.

Ajeet Khurana, the head of the India’s blockchain and cryptocurrency committee, told the YourStory website, the government, like all governments in the world apart from Japan, did not recognise cryptocurrency as money. Many websites have been reporting, falsely, that Indian Finance Minister Arun Jaitley told parliament while presenting the national budget that India would make cryptocurrencies illegal.

Locally, Assistant Treasurer Michael Sukkar, speaking at a financial services briefing on Wednesday night, confirmed the Turnbull government is investigating how it could tax digital currencies like bitcoin.

In the U.S., Bank of America is now the largest lender barring customers from using credit cards to buy cryptocurrencies. According to Bloomberg, the policy was made known to employees yesterday and took effect today. Neither Discover nor Capital One allow crypto transactions on their cards. JPMorgan still does.

Alan Greenspan, the former Fed Chair, speaking on Wednesday on Bloomberg Television said “there are two bubbles: We have a stock market bubble, and we have a bond market bubble”.

This at a time when US stock indexes remain near record highs and as the yields on government notes and bonds hover not far from historic lows.

As the Fed continues to tighten monetary policy, interest rates are expected to move up in coming years.

At the end of the day, the bond market bubble will eventually be the critical issue, but for the short term it’s not too bad

But we’re working, obviously, toward a major increase in long-term interest rates, and that has a very important impact, as you know, on the whole structure of the economy.

What’s behind the bubble? Well the fact, that, essentially, we’re beginning to run an ever-larger government deficit.

Greenspan said. As a share of GDP, “debt has been rising very significantly” and “we’re just not paying enough attention to that.”

The Fed held their target range but confirmed its intent to lift rates ahead at Yellen’s last meeting as head. The bank signalled that it would push ahead on its monetary policy tightening path as economic activity has been rising at a solid rate, while inflation remained low but is expected to “move up” in the coming months. Most analysts suggest 2-3 hikes this year. The T10 bond yield continues to rise and is highest since 2014. Expect rates to go higher, putting more pressure on international funding costs.

Information received since the Federal Open Market Committee met in December indicates that the labor market has continued to strengthen and that economic activity has been rising at a solid rate. Gains in employment, household spending, and business fixed investment have been solid, and the unemployment rate has stayed low. On a 12-month basis, both overall inflation and inflation for items other than food and energy have continued to run below 2 percent. Market-based measures of inflation compensation have increased in recent months but remain low; survey-based measures of longer-term inflation expectations are little changed, on balance.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee expects that, with further gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace and labor market conditions will remain strong. Inflation on a 12‑month basis is expected to move up this year and to stabilize around the Committee’s 2 percent objective over the medium term. Near-term risks to the economic outlook appear roughly balanced, but the Committee is monitoring inflation developments closely.

In view of realized and expected labor market conditions and inflation, the Committee decided to maintain the target range for the federal funds rate at 1-1/4 to 1‑1/2 percent. The stance of monetary policy remains accommodative, thereby supporting strong labor market conditions and a sustained return to 2 percent inflation.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments. The Committee will carefully monitor actual and expected inflation developments relative to its symmetric inflation goal. The Committee expects that economic conditions will evolve in a manner that will warrant further gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data.

Just 24 hours after the announcement of a new CEO, when we were assured that CBA were well on the way to addressing their known issues; ASIC lobbed a bombshell in the shape of the BBSW case.

CBA said today:

Commonwealth Bank has fully co-operated with ASIC’s investigation over the last two years.

Commonwealth Bank disputes the allegations made by ASIC. As this matter is before the courts, it is not appropriate to comment further at this time.

Put to one side whether CBA was part of the group of banks that fixed the pricing of BBSW, and the knock-on effect on product pricing; surely this issue was on the “risk” list in the bank, and should have been disclosed.

If it was not, it should have been. This may once again speak to cultural issues in the organisation. There is clearly much to fix. What else is on the risk list?

More broadly, we have to consider whether the sheer complexity of the organisation is part of the problem. Perhaps CBA should be split into a series of small entities, for example, separated into its retail division, corporate, wealth, insurance and trading divisions. The question of whether CBA is simply too big and complex to manage, is in our view the underlying and most critical question to be addressed.

ASIC has today commenced legal proceedings in the Federal Court in Melbourne against the Commonwealth Bank of Australia (CBA) for unconscionable conduct and market manipulation in relation to CBA’s involvement in setting the bank bill swap reference rate (BBSW) between 31 January 2012 and October 2012.

The BBSW is the primary interest rate benchmark used in Australian financial markets and was administered by the Australian Financial Markets Association (AFMA) during the relevant period. On 27 September 2013, AFMA changed the method by which the BBSW is calculated. The conduct that the proceedings relate to occurred before this change in methodology. Since 1 January 2017 ASX Limited has been the administrator of the BBSW, introducing a new Volume Weight Average Price (VWAP) based calculation methodology.

During the relevant period CBA had a large number of products which were priced or valued off BBSW. ASIC alleges that on three specific occasions CBA traded with the intention of affecting the level at which BBSW was set so as to maximise its profits or minimise its losses to the detriment of those holding opposite positions to CBA’s.

ASIC alleges it was unconscionable for CBA to trade in this way, and also to enter into products priced off the BBSW without disclosing its trading practices to its customers and counterparties. ASIC also alleges that CBA’s trading created an artificial price and a false appearance with respect to the market for some of these products.

ASIC is seeking declarations that CBA contravened s12CA, s12CB, s12DA, 12DB and s12DF of the Australian Securities and Investments Commission Act 2001 (Cth) (ASIC Act), s912A(1), s1041A, s1041B and s1041H of the Corporations Act 2001 (Cth) (Corporations Act).

Further, ASIC has sought from the Court pecuniary penalties against CBA and an order requiring CBA to implement a compliance program.

ASIC will be making no further comment at this time.

ASIC commenced legal proceedings in the Federal Court against the Australia and New Zealand Banking Group (ANZ) on 4 March 2016 (refer: 16-060MR) and against National Australia Bank (NAB) on 7 June 2016 (refer: 16-183MR).

On 10 November 2017, the Federal Court made declarations that each of ANZ and NAB had attempted to engage in unconscionable conduct in attempting to seek to change where the BBSW set on certain dates and that each bank failed to do all things necessary to ensure that they provided financial services honestly and fairly. The Federal Court imposed pecuniary penalties of $10 million on each bank (refer: [2017] FCA 1338).

On 20 November 2017, ASIC accepted enforceable undertakings from ANZ and NAB which provides for both banks to take certain steps and to pay $20 million to be applied to the benefit of the community, and that each will pay $20 million towards ASIC’s investigation and other costs (refer: 17-393MR).

On 5 April 2016, ASIC commenced legal proceedings in the Federal Court against the Westpac Banking Corporation (Westpac) (refer: 16-110MR). The matter is awaiting judgment.

ASIC has previously accepted enforceable undertakings relating to BBSW from UBS-AG, BNP Paribas and the Royal Bank of Scotland (refer: 13-366MR, 14-014MR, 14-169MR). The institutions also made voluntary contributions totaling $3.6 million to fund independent financial literacy projects in Australia.

In July 2015, ASIC published Report 440, which addresses the potential manipulation of financial benchmarks and related conduct issues.

The Government has recently introduced legislation to implement financial benchmark regulatory reform and ASIC has consulted on proposed financial benchmark rules.

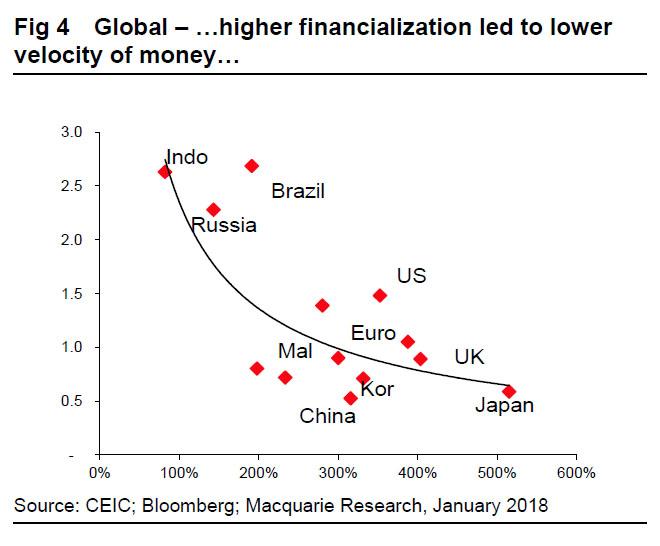

Investors are currently residing in a surreal world of low volatilities and spreads, ignoring potentially radical shifts in monetary and fiscal policies and unwinding of extraordinary measures of the last decade. Even as Central Banks (CBs) are worried about lack of volatility and excessive risk-taking, investors seem convinced that either strength of economic recovery, or return to liquidity and cost of capital supports, will ensure that volatilities are kept under control. Thus, either way, investors seem to expect that spreads would stay low and elevated valuations of various asset classes remain a permanent feature of an investment landscape.

Do we agree? In our view, financial markets have been for years drifting away from real economies. Not only is the value of financial assets at least five-to-ten times larger than the underlying economies, but also this ‘financial cloud’ is now managed by computer trading, algorithms, AI and passive investments.

This is potentially a highly destabilizing mix.

CBs are aware of dangers; hence the warnings by IMF and BIS to be ‘mindful’ of gaps between economic growth and asset bubbles. In our view, CBs and financial supervisory bodies have essentially morphed from masters of the universe into slaves of grotesquely swollen financial markets.

The key to monetary policy is no longer to guide real economies, but to avoid a collapse of the financial cloud, out of fear of what a return to traditional price discovery and volatilities might imply for wealth creation and asset prices. Over the last three decades, real economies (everything from personal savings to fixed-asset investment) have become far more tightly intertwined with asset values than with wages or productivity.

In this surreal world of complete dominance of financial assets, conventional economic rules break down and financialization and avoidance of sharp asset price contractions becomes the paramount policy objective. In our view, this implies that liquidity supports cannot be withdrawn and cost of capital (holistically defined) can never rise.

Only a return to private sector dominance and accelerating productivity (rather than recoveries driven by liquidity and/or stimulus) can ensure ‘beautiful deleveraging’. We maintain that this remains a low-probability event.

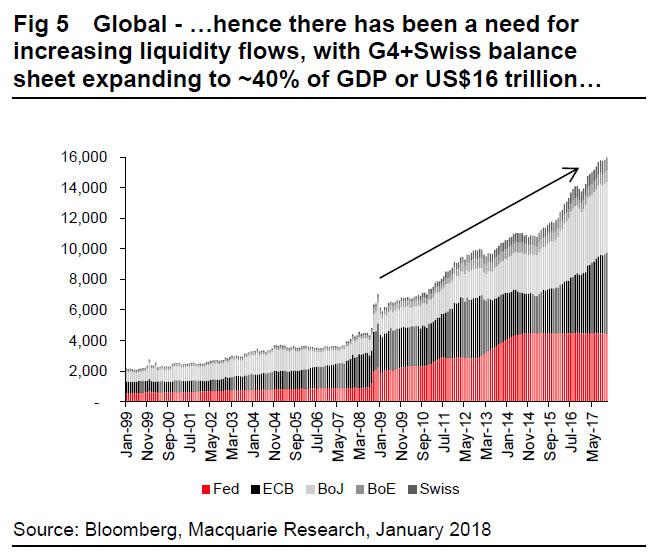

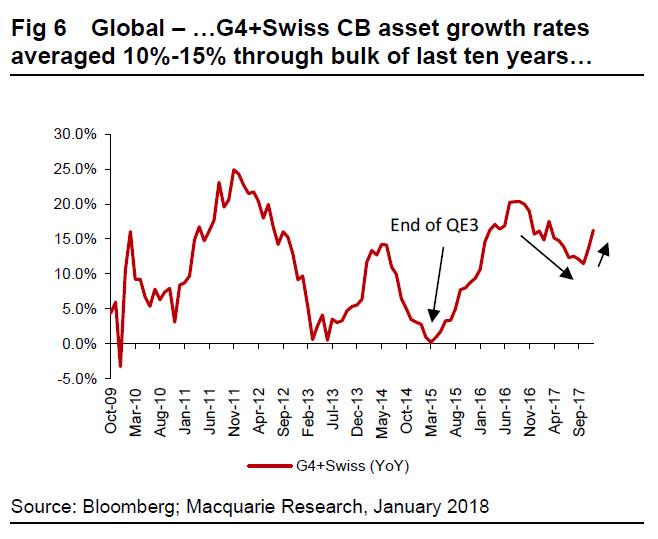

Far more likely is that the latest two-year-old recovery was due to a mix of unique and to some extent unsustainable factors, such as massive liquidity injections by key CBs (US$3.5 trillion – Mar’16 and Dec’17), coordinated monetary policies (since Feb’16) and as always, China’s stimulus.

The question therefore is what would happen to values and volatilities, if these three supports are gradually withdrawn. For example, CBs’ liquidity injection in ’18 is likely to be only ~US$0.7 trillion (turning negative in ’19) or growth of ~5%, barely enough to cover global nominal GDP (~6%).

Similarly, CBs are likely to make repeated attempts to raise cost of capital, despite likely inability to do so while China is tightening, and if history is any guide, it would more than likely over-tighten. This should raise volatilities. Even if assume that recovery is indeed more sustainable, CBs (uncomfortable as they are with current excessive valuations and low volatilities) would be happy to see volatilities rise and return to some form of price discovery. The 64-dollar dollar question is whether ‘patient is sufficiently healthy to withstand pressure’.

Thus, one way or another, it seems volatilities are likely to rise at some point in ’18, and as always ‘canary’ in the coalmine would be high yield, FX and EM markets.

The U.S. Securities and Exchange Commission Chairman Jay Clayton spoke at Stanford University’s Stanford Rock Center for Corporate Governance and discussed his first eight months at the SEC and his enforcement, examination, market, and capital formation priorities. His comments on cryptocurriences were revealing.

SEC is clearly monitoring Initial Coin Offers (ICO) , and is concerned about the lack of protection for investors. There is significant risk of price manipulation, yet the underlying blockchain technologies offer significant opportunity.

“What I see happening in the ICO market today is ‘let me have all of the disclosure freedom of a private placement and all of the secondary activity and ability to market this of a public offering. We decided in 1934: that [having both of these at once] led to a lot of problems.”

“I think we can say that wherever the date is, it’s passed,” he said when asked whether his commission has made ICO rules clear enough yet.

“There are a lot of protections in the way stock trades on exchanges… these platforms that you’re seeing where people are trading cryptocurrencies — there are none of these rules… The opportunity for price manipulation is at orders of magnitude.”

“Blockchain, distributed ledger tech — I don’t think any of us think it’s a fad… it clearly has a applications that are gonna add efficiencies.”

“If this market continues as it is, this will not be the last enforcement actions that we take,” he said of the three ICOs the S.E.C. has moved against so far.

“Some of the offerings that we’re seeing, if the lawyers are telling them it’s OK, they’re just plain wrong,” he said, adding that taking action against lawyers knowing giving advice to ICO issuers that is against current laws is a possibility.